Preface

Why measure impact?

Faced with environmental and social urgency, investors are increasingly expected to demonstrate the effectiveness of their investments beyond financial performance alone. Measuring extra-financial dimensions provides tangible evidence of the positive effects generated, so as to meet the expectations of clients, regulators and civil society. Indeed, measuring what companies produce for society and the planet is indispensable to managing those effects and improving them. This requirement is part of the impact-finance approach, defined by the Institut de la Finance Durable as an investment strategy that aims to accelerate the just and sustainable transition of the real economy by providing evidence of its beneficial effects.

Mirova has therefore developed a rigorous framework to assess the exposure and effective contribution of its funds to the environmental and social transition. The framework rests on the DNA of impact investing — intentionality, additionality and measurability — as promoted in particular by the Forum pour l’Investissement Responsable (FIR), France Invest and the Institut de la Finance Durable (IFD). The objective is two fold : to steer the strategy according tothe extra-financial results obtained, and to demonstrate these results in an accessible way to internal and external audiences.

IN BRIEF

This note distinguishes three complementary concepts — the impact of the underlying assets, the fund's financial exposure to those impacts through its investments, and the investor's real contribution (additionality) — and unfolds them across five levels of analysis, from the assets financed to investor additionality.

This detailed version, produced by the Mirova Research Center, is the subject of a summary note published by Mirova : the two documents are complementary and mirror one another.

Overview

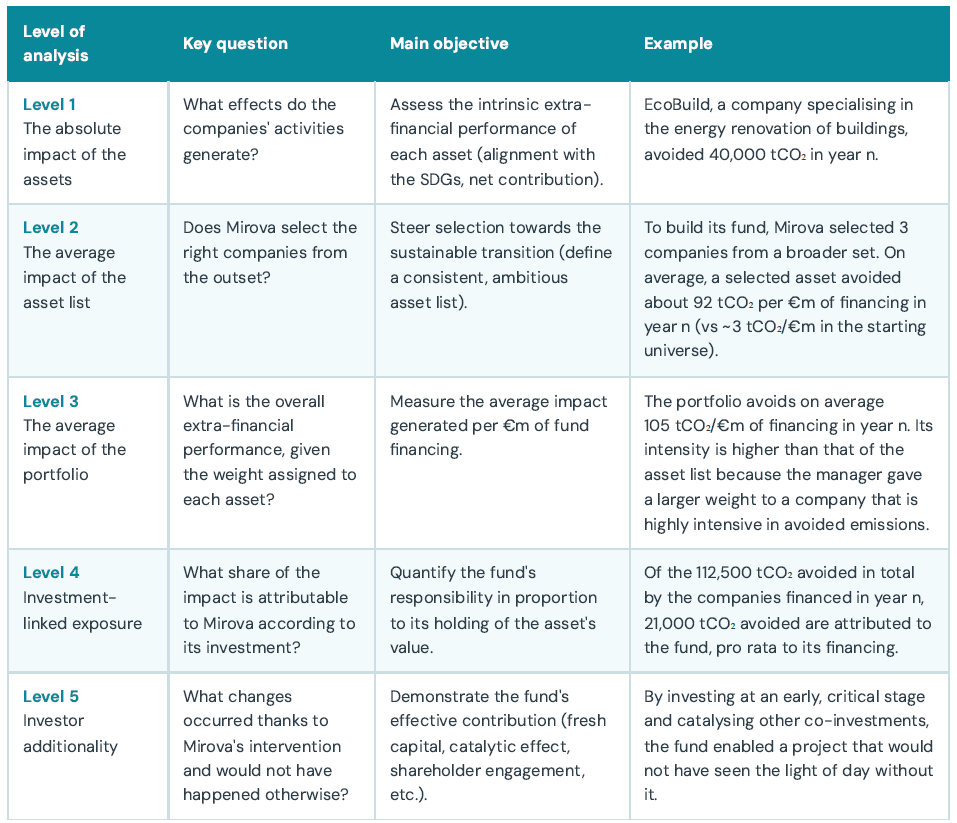

Our five-level analytical framework

To address these challenges, we propose a multi-level approach that distinguishes three complementary concepts : the impact of the underlying assets, the fund's financial exposure to those impacts through its investments, and finally the investor's real contribution — or additionality. This approach is structured in five complementary levels, from the assets financed toinvestor additionality.

Introduction

Key concepts : impact, exposure and real contribution

Many indicators used in sustainable finance primarily describe the extra-financial performance of the underlying assets (green companies, social projects, etc.). They measure the environmental or social effects generated by the activities financed. However, these indicators are not sufficient to characterise an investor's role : they say nothing about how capital is allocated within the portfolio,nor about the specific effects of the investor's intervention. Three key notions must therefore be clearly distinguished : the impact of the underlying assets, a portfolio's exposure to activities with environmental and/or social impact, and its real contribution to the changes observed (additionality).

- Asset impact corresponds to the environmental or social effects generated by the companies or projects financed, independently of the investor's role. It measures what the company's or project'sactivities produce : avoided emissions, jobs created, beneficiaries reached, improved access toessential services, etc. It does not make it possible to determine what share of that impact is linked tothe fund's financing, nor whether that financing played a causal role.

- Exposure describes what the fund invests in and in what proportions. It thus reflects the portfolio'salignment with certain environmental or social activities. For example, a fund invested 100% in renewable energy will show a low carbon footprint and a high proportion of "green" assets, indicating that the portfolio is largely exposed to positive-impact activities. Unlike companies' absolute impact indicators, exposure takes into account the amounts actually invested in each asset. A fund may indeed invest very different amounts in the companies it finances : it can be heavily exposed to companies with poor practices and, conversely, invest only marginally in companies that are highly virtuous from an environmental or social standpoint. Absolute impact indicators, when simply aggregated, therefore reflect neither how the portfolio is actually built nor the investor's capital-allocation choices — which exposure captures better.

- The fund's real contribution, or additionality, seeks to determine the extent to which the investor's intervention generated additional impact. The question then becomes : what changed thanks to the fund's intervention? A company may generate positive impacts independently of the fund investing in it, or could have obtained financing from other players; the investor is then exposed to an existing impact without necessarily being at its origin. Conversely, when the fund's financing enables a project to happen or accelerate — for example by investing at an early stage in a renewable-energy project that would not otherwise have seen the light of day — it effectively contributes to creating additional impact : the portfolio increased positive impact or avoided negative impact, relative to what would have happened anyway. That is a real contribution of the fund itself.

The three approaches are complementary. Asset impact is the starting point : for a fund to claim tofinance positive impacts, the assets it invests in must themselves generate such impacts. Moreover, strong exposure to sustainable activities is generally a prerequisite for claiming positive impact — it is difficult, for example, to have a positive environmental impact while mostly financing fossil fuels.However, strong exposure is not a sufficient condition for investor additionality; conversely, an investor can make a decisive contribution with relatively limited capital, if its intervention was crucial to enabling or accelerating a project.

Recognising the distinction between exposure and the fund's real contribution avoids two pitfalls :overestimating impact, or overclaiming (by conflating the exposure and the contribution of a"green" portfolio built through selection), and underestimating the additionality brought by certain engaged investors.

Mirova has therefore structured its environmental and social performance measurement framework along a multi-level logic, from the micro level (the assets in the portfolio) to the macro level (the fund and its additionality), in order to assess impact from different angles. The five levels of analysis retained are : the assets, the asset list, the portfolio, the investment and investor additionality. Each provides a specific perspective, with its own methodologies, objectives and limitations, which we detail below.

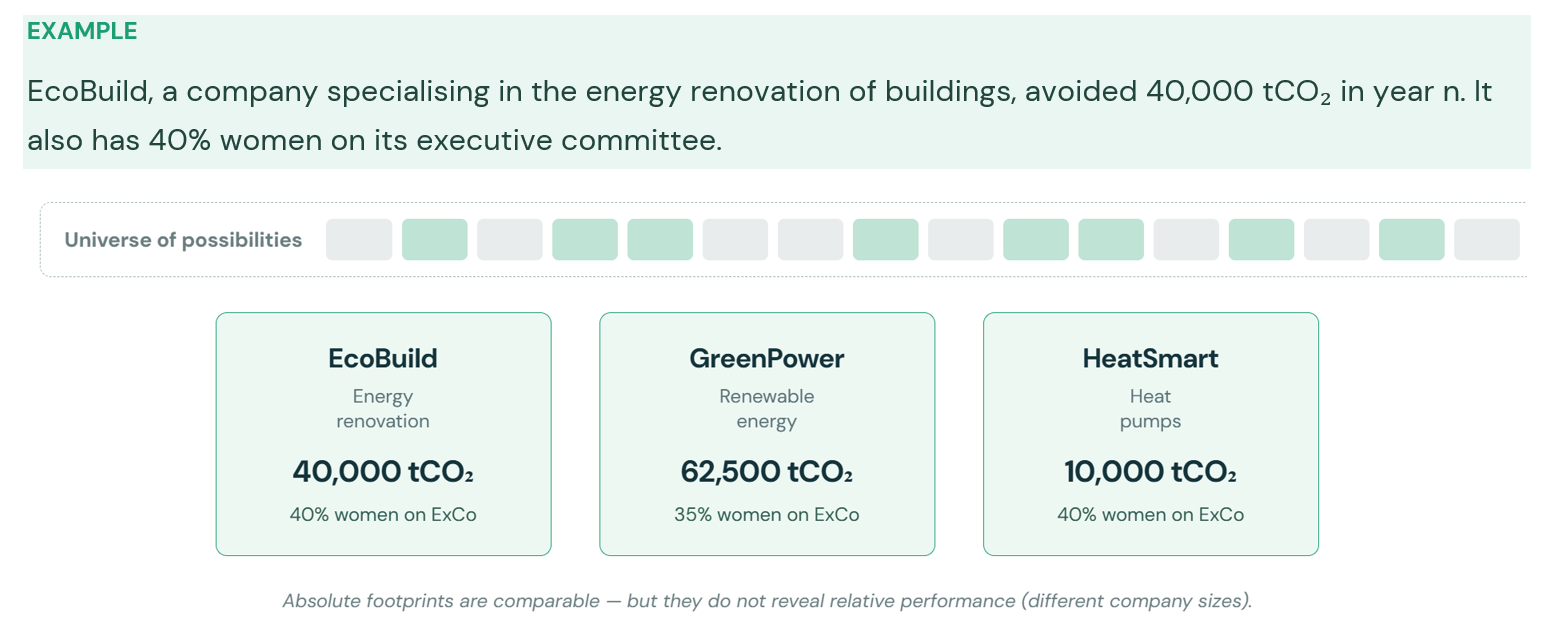

Level 1 - The absolute impact of the assets

What impact do the activities generate, independently of any portfolio?

This first level assesses the intrinsic impact of each asset, independently of any portfolio or financing consideration. We take the company's (or project's) point of view : what environmental and social effects does it produce through its activity?

Each asset is assigned an overall impact opinion, on a qualitative scale ranging from "negative impact" to "strong positive impact", reflecting its degree of contribution to the Sustainable Development Goals. This assessment takes into account the share of revenue dedicated to sustainable solutions, the quality of ESG practices and the positive or negative externalities generated. On the quantitative side, the absolute indicators measured may include tonnes of CO₂ avoided annually, the number of beneficiaries reached, hectares of biodiversity preserved or jobs supported.

As they stand, these absolute footprints are comparable, but they do not reveal the companies' relative performance : a larger company naturally produces more effects, without this necessarily reflecting better performance. That is precisely the motivation for the next level.

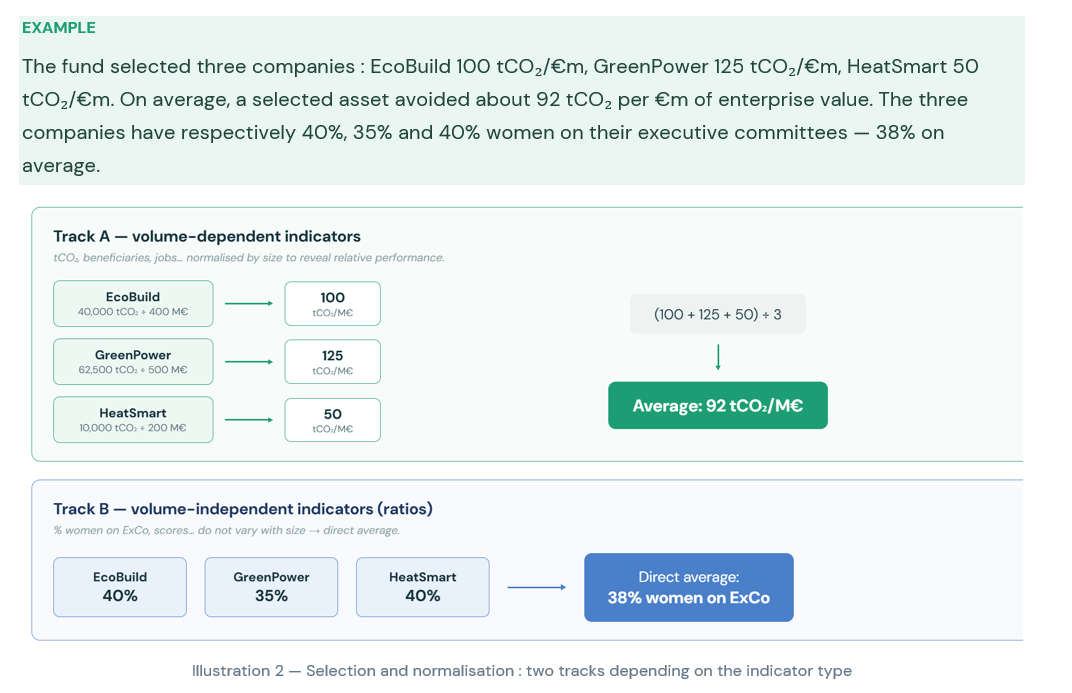

Level 2 - The average impact of the asset list

Is the selection of assets consistent with our impact objectives?

This second level reflects the selection choices made by the manager within an investment universe. It measures the average impact of the assets retained. At this stage it is not yet a portfolio : all assets are considered at equal weight, in order to assess the average quality of the selection — the "selection effect".

Two methodological tracks coexist depending on the nature of the indicators : volume-dependent indicators are first normalised by an economic dimension (revenue, enterprise value) and then averaged; volume-independent indicators (percentages, scores) are averaged directly.

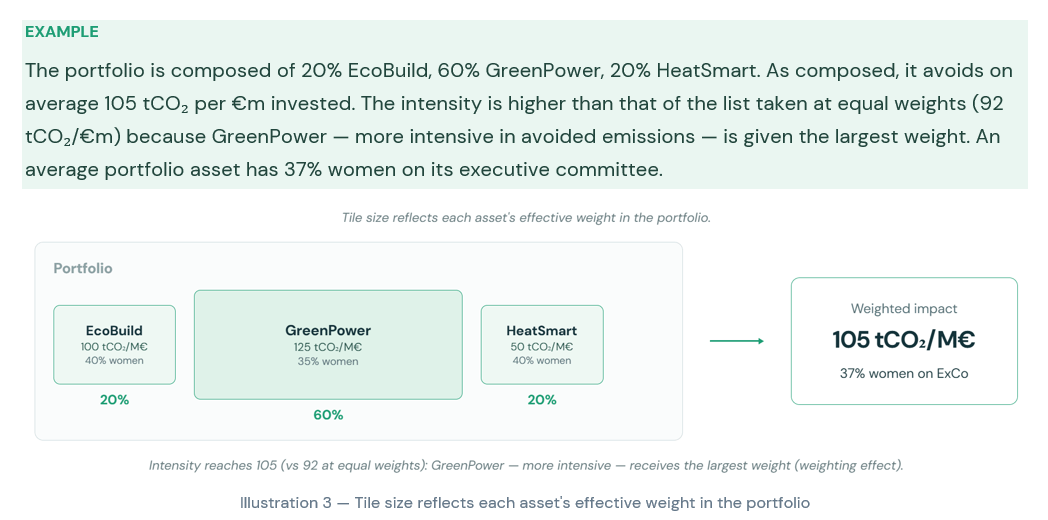

Level 3 - The average impact of the portfolio

What is the average impact of the portfolio as actually composed?

This third level measures the extra-financial performance of the portfolio actually built, taking into account the weights assigned to each asset. Performance is now expressed per million euros invested — no longer financed by all of the company's financiers (level 2), but invested in the portfolio. This level directly reflects the manager's allocation choices : it is the "weighting effect".

Level 4 - Investment-linked exposure

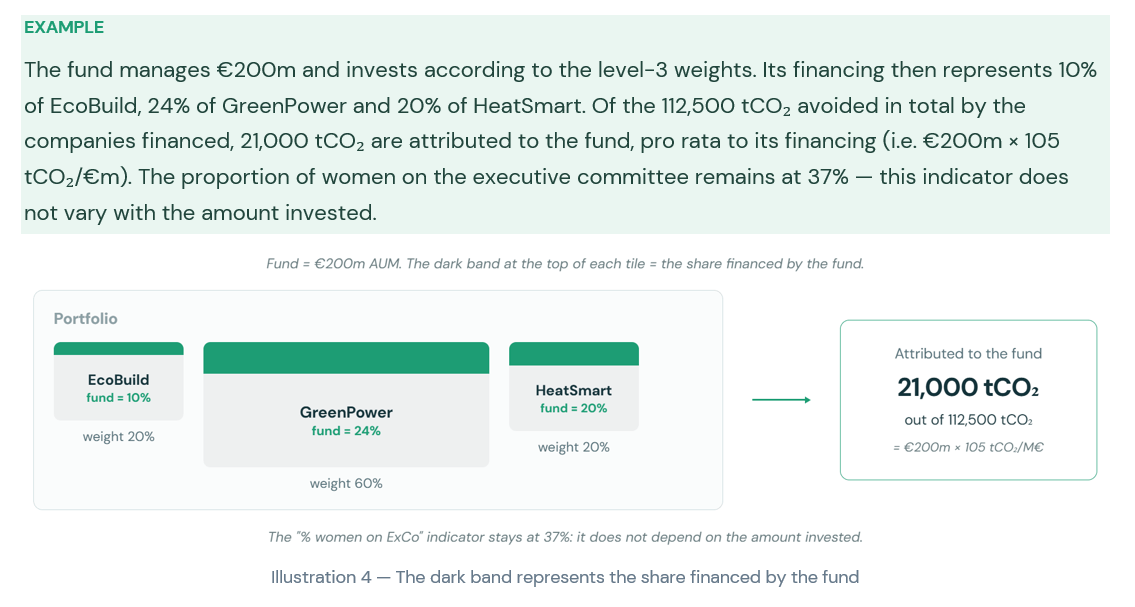

What share of the assets' impact is attributable to the fund, pro rata to its financing?

This fourth level attributes a share of the impacts generated by the underlying companies to their respective financiers — and in particular to the fund — according to its financing contribution. It represents the impacts financed by the fund, but does not prejudge the investor's causal role, which belongs to the next level.

Attribution applies only to indicators that vary with the volume of financing. Structural indicators (share of women on the executive committee, scores) remain identical to those of level 3 : they do not depend on the amount invested.

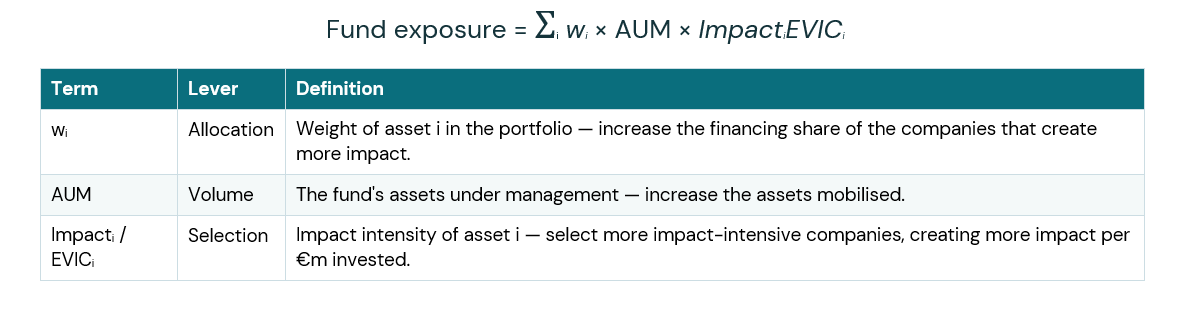

The investor's levers for action

Once impacts are measured and attributed at fund level, the equation below decomposes total impact into several distinct terms, which make it possible to analyse, steer and compare impact-investing strategies.

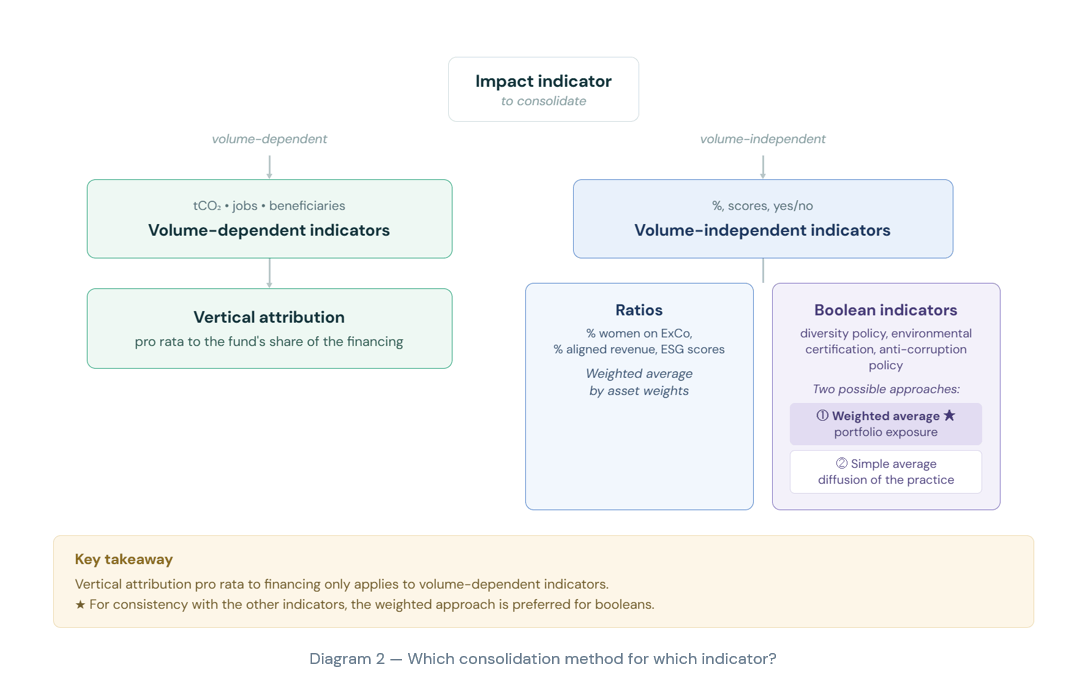

In practice: which consolidation method?

Indicators are consolidated at portfolio and fund level following two distinct logics, which stem from whether or not they depend on activity volume. Absolute impact indicators (CO₂ emissions avoided, jobs supported, beneficiaries reached) can be attributed to the fund following a vertical-attribution logic, according to its share in the financing of the assets : this is the family that lends itself to measuring the fund's own contribution.

Volume-independent indicators vary neither with company size nor with financing : they reflect a structural characteristic and therefore do not lend themselves to pro-rata attribution, but remain essential for analysing the composition of the portfolio. Ratios are aggregated through weighted averages based on asset weights; boolean indicators can be consolidated either through a weighted average (the portfolio's effective exposure) or a simple average (the diffusion of a practice). For consistency with the other indicators, we favour the first approach

Level 5 - Investor additionality

What would not have happened without the investor?

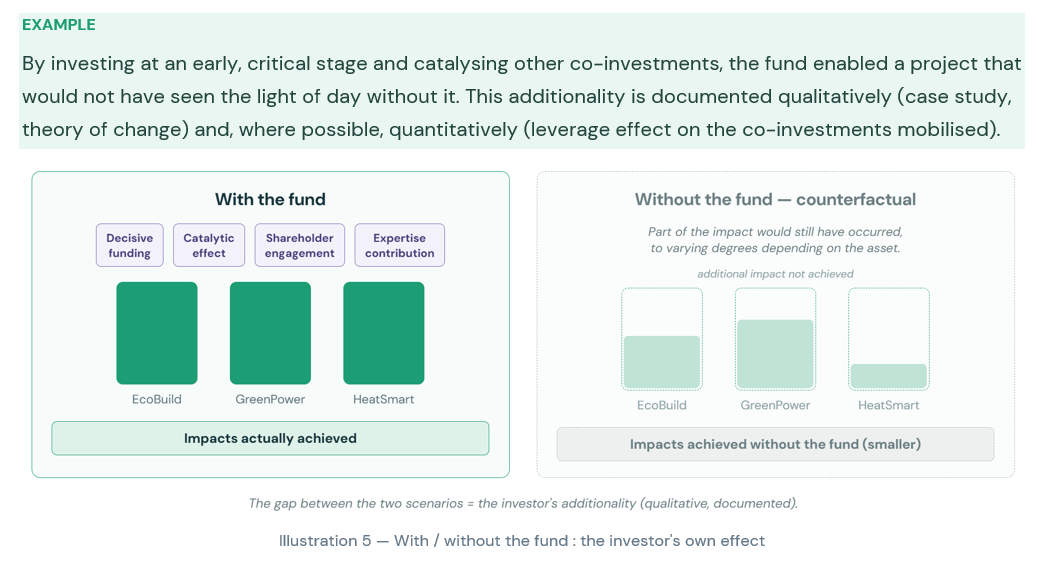

This fifth level assesses the investor's additionality, i.e. the effects that occurred thanks to its action and would not have happened in its absence. The aim is to go beyond financial attribution and characterise the active role played by the investor — decisive financing, catalytic effect, shareholder engagement, contribution of expertise.

This level necessarily rests on a qualitative, documented and transparent approach. It is the most demanding, but also the most decisive for judging a fund's true contribution to the transition.

Conclusion

A tool for steering

Measuring the impact of underlying assets and funds is an essential exercise for steering impact investing and making it credible — but it must be accompanied by humility and critical thinking.

The framework presented offers a solid basis for assessing, improving and communicating the impact of our funds. The ultimate challenge is to convert these measurements into concrete levers for action : adjusting investment strategies according to the results observed, strengthening our engagements where the indicators reveal gaps, and directing more capital towards the most effective solutions.

In this sense, impact measurement — far from being one more reporting constraint — becomes a strategic tool in service of the transition.